Executive Summary

- Strategic securitization offers a potent mechanism for transforming income-contingent academic liabilities into marketable financial instruments.

- This approach promises enhanced fiscal stability for governments, diversified investment opportunities, and improved liquidity within educational finance.

- Careful structural design, robust risk mitigation, and stringent regulatory oversight remain paramount for market integrity and stakeholder protection.

The burgeoning landscape of higher education finance presents unique fiscal challenges. Income-contingent repayment (ICR) programs, while socially equitable, introduce significant uncertainty into government balance sheets. These liabilities impede fiscal velocity. Innovative financial engineering is therefore crucial. Strategic securitization emerges as a powerful solution. This sophisticated approach transforms unpredictable future cash flows into tradable assets. It unlocks capital. This benefits all market participants.

Deconstructing Income-Contingent Academic Liabilities

Income-contingent repayment plans link loan obligations directly to borrower earnings. This provides a vital safety net for graduates. However, it creates an actuarial challenge. Future revenue streams become highly volatile. This volatility stems from individual career trajectories. Macroeconomic conditions also play a significant role. Unemployment rates, wage growth, and economic downturns directly impact repayment capacity. These factors introduce substantial fiscal uncertainty for the government. It holds these non-standardized financial instruments.

Traditional fixed-payment loans offer predictable amortization schedules. ICR loans diverge fundamentally. Their repayment profiles are stochastic. This complicates financial forecasting. It also makes capital allocation difficult. The government effectively acts as a long-term risk absorber. This can strain public finances. Managing this expansive portfolio requires novel strategies. Securitization provides a structural answer. It transfers this inherent variability to capital markets. This distributes risk more broadly.

Income-contingent repayment models, while progressive, introduce complex cash flow analytics. Their intrinsic volatility poses a persistent challenge for public finance departments seeking budgetary predictability. Strategic financial structuring is imperative.

The Mechanics of Securitization in Education Finance

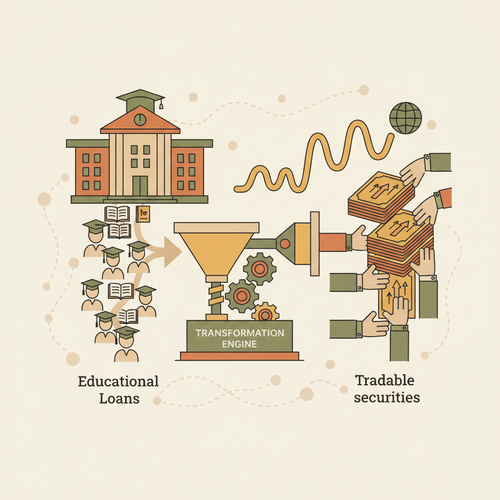

Securitization involves pooling illiquid assets into a single financial instrument. These pooled assets then generate cash flows. These cash flows service new securities. For ICR liabilities, this process aggregates thousands of individual loan contracts. These form a larger, more predictable payment stream. This stream underpins the issuance of new asset-backed securities. These are often termed Student Loan Asset-Backed Securities (SLABS). These instruments are then sold to institutional investors.

The process begins with an originator. This entity typically manages the original loan portfolio. A special purpose vehicle (SPV) is then created. This SPV purchases the loans from the originator. The SPV isolates these assets from the originator’s balance sheet. This prevents commingling risks. The SPV subsequently issues various classes, or tranches, of securities. Each tranche carries different risk and return profiles. This caters to diverse investor appetites. Credit rating agencies assess these tranches. They assign ratings based on perceived credit quality and structural enhancements.

Crucially, a servicer manages the ongoing collection of payments. The servicer ensures compliance with ICR terms. This includes income verification and payment adjustments. Investor confidence hinges on robust servicing. Efficient servicing minimizes default rates. It optimizes cash flow capture. This entire ecosystem facilitates a critical liquidity injection. It converts a long-term, illiquid asset into capital market instruments. This enhances fiscal maneuverability for the government.

Investor Value Proposition and Market Dynamics

Income-contingent academic liability securitization offers compelling advantages for investors. These securities often feature implicit or explicit government backing. This significantly reduces credit risk. Such backing enhances their attractiveness. This creates a stable, high-quality asset class. Investors seeking fixed-income diversification find these instruments appealing. They offer an alternative to traditional corporate or sovereign debt. Their performance is less correlated with other asset classes. This provides valuable portfolio diversification.

The structured nature of SLABS allows for yield enhancement. Different tranches can appeal to varying risk preferences. Senior tranches typically offer lower yields but higher security. Mezzanine and equity tranches carry higher risk. They compensate with potentially greater returns. This stratification attracts a broad investor base. Pension funds, insurance companies, and asset managers actively seek such structured products. They offer predictable cash flows over extended periods. This aligns well with long-term liability matching strategies.

Furthermore, these instruments offer an inflation hedge. Loan repayments adjust with borrower income. Income typically correlates with inflation. This provides a natural protection against purchasing power erosion. The social impact component also draws certain investors. Environmental, Social, and Governance (ESG) mandates increasingly guide investment decisions. Investing in education-backed assets aligns with social impact objectives. This broadens the investor pool. It contributes to robust market demand.

Mitigating Systemic Risks and Enhancing Credit Quality

Robust risk mitigation is paramount in any securitization framework. Especially with income-contingent liabilities. Overcollateralization serves as a primary credit enhancement. The value of the pooled loans exceeds the issued securities. This provides a buffer against defaults. Subordination also plays a critical role. Junior tranches absorb initial losses. This protects senior tranche investors. Government guarantees, explicit or implicit, further bolster creditworthiness. These assurances reduce investor apprehension significantly.

Addressing moral hazard is crucial. Borrowers might strategically underreport income. They might also pursue lower-paying jobs. This would minimize repayment obligations. Stringent verification processes are indispensable. Regular income recertification combats this. Public awareness campaigns also reinforce repayment ethics. Adverse selection risk must also be managed. Only higher-risk borrowers might choose ICR options. This could skew the underlying asset pool. Sophisticated actuarial modeling identifies these risks early. It informs appropriate pricing adjustments.

Effective servicer performance is non-negotiable. The servicer directly impacts cash flow generation. High-quality servicing minimizes delinquencies. It maximizes recovery rates. Key performance indicators (KPIs) for servicers are essential. These include collection efficiency and borrower satisfaction. Independent audits ensure servicer accountability. Transparency in reporting and robust legal frameworks reinforce investor confidence. These measures collectively strengthen the credit quality of the securitized assets. They reduce the potential for systemic instability.

Expert Insight: Effective risk layering through subordination and overcollateralization is non-negotiable. Furthermore, a meticulously designed servicing framework directly correlates with the long-term performance and market liquidity of these complex instruments.

Macroeconomic Impacts and Fiscal Deleveraging

Securitizing income-contingent academic liabilities can have profound macroeconomic effects. For governments, it represents a significant opportunity for fiscal deleveraging. By converting illiquid, uncertain assets into marketable securities, governments can reduce their outstanding debt. This frees up budgetary resources. These resources can then be redirected. They can fund critical public services. Alternatively, they can reduce taxes. This stimulates broader economic activity. It improves fiscal health. This enhances sovereign credit ratings. It lowers borrowing costs.

The infusion of capital into higher education systems is another critical outcome. Governments might utilize proceeds from securitization. This could fund new educational initiatives. It could expand access. It could also reduce tuition burdens. This can enhance human capital development. A more educated workforce fuels innovation. It drives productivity growth. This has long-term positive economic ramifications. It creates a virtuous cycle. Educational attainment directly correlates with economic prosperity.

Furthermore, this financial innovation can stabilize consumer spending. Reduced government fiscal pressure mitigates the need for future austerity measures. This fosters greater consumer confidence. Lower student debt burdens through efficient market mechanisms could also free up household income. This boosts discretionary spending. It stimulates aggregate demand. Careful implementation ensures a net positive macroeconomic impact. It avoids unintended consequences or market distortions. This requires continuous monitoring. It needs adaptive policy adjustments.

Regulatory Frameworks and Policy Imperatives

A robust regulatory framework is indispensable for the integrity of this market. It protects all stakeholders. Transparent disclosure requirements are fundamental. Investors need comprehensive information. This includes loan pool characteristics, servicing agreements, and risk factors. Standardized reporting metrics enhance comparability. They foster informed investment decisions. Strong oversight prevents predatory practices. It ensures fair treatment for borrowers. This builds trust in the asset class.

Consumer protection remains a primary policy imperative. Clear communication about repayment terms is vital. Access to financial counseling supports borrowers. Mechanisms for dispute resolution are also essential. Regulations must strike a delicate balance. They must facilitate market efficiency. Simultaneously, they must safeguard vulnerable individuals. This balance ensures social equity. It prevents potential exploitation. Regulatory arbitrage must be vigilantly avoided.

International best practices provide valuable guidance. Harmonizing standards can foster cross-border investment. It can expand market liquidity. Collaboration between financial regulators and educational bodies is crucial. This integrated approach addresses both market stability and social welfare objectives. Adaptive regulatory responses are necessary. The financial landscape constantly evolves. Emerging risks demand proactive policy adjustments. This proactive stance ensures market resilience. It sustains long-term growth.

Learn more about securitization on Investopedia.

Future Trajectories and Innovations in Academic Asset-Backed Markets

The securitization of income-contingent academic liabilities is poised for further evolution. Advanced data analytics and machine learning (AI/ML) will revolutionize risk assessment. Predictive models will forecast default rates with greater accuracy. They will also project income trajectories. This refines credit enhancement strategies. It optimizes tranche structuring. Such technological integration will enhance market efficiency. It will attract even more sophisticated institutional capital.

Innovative product structures are likely to emerge. These might include outcome-based financing. Here, investor returns correlate with graduate employment success. Public-private partnerships could also become more prevalent. These models share risk and reward between government and private capital. This incentivizes better educational outcomes. It drives efficiency. This collaborative approach leverages diverse expertise. It mobilizes additional funding sources.

The global expansion of these markets presents significant opportunities. Developing economies face similar educational funding challenges. Adapting securitization models to diverse regulatory and cultural contexts is key. Standardized legal frameworks will facilitate this expansion. Benchmarking against established asset-backed markets will provide valuable insights. The long-term trend points toward increasing sophistication. It moves toward greater market integration. This offers significant potential for sustainable educational finance. It contributes to global economic stability.

Explore Income-Contingent Repayment Plans in detail.

Conclusion

Strategic securitization of income-contingent academic liabilities represents a significant financial innovation. It addresses critical challenges in educational funding. This mechanism transforms unpredictable future income streams into valuable capital market assets. It offers clear benefits to governments, investors, and students. Prudent design and diligent oversight remain fundamental. These ensure market integrity. They protect borrower interests. The long-term fiscal health of nations hinges on such forward-thinking financial solutions.

Are we sufficiently leveraging capital markets to foster accessible, sustainable higher education globally?